June CPI Report and Fed Chair Warsh Testimony to Shape Rate Outlook

Tuesday's inflation data and Fed Chair Kevin Warsh's Capitol Hill testimony could reset market expectations for interest rates and dollar direction.

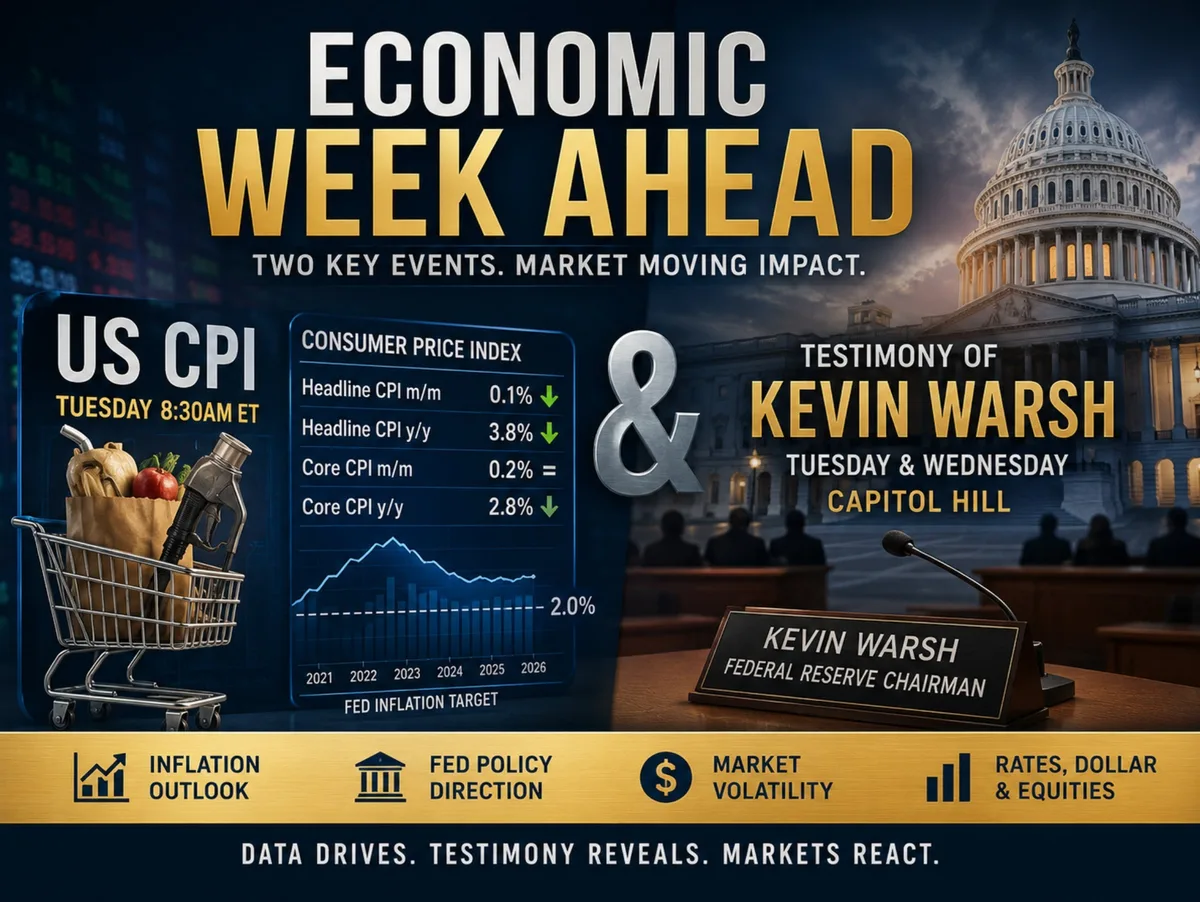

Two events this week carry the weight of potential policy pivots: Tuesday's June CPI release and Federal Reserve Chairman Kevin Warsh's semiannual congressional testimony. Together, they represent the most concentrated risk for markets — spanning the dollar, Treasuries, equities, and gold — in recent memory. The sequencing matters: fresh inflation data will land two hours before Warsh faces lawmakers, meaning markets will have an immediate interpretive lens through which to filter everything he says.

Economists expect headline CPI to rise just 0.1% month-over-month, the softest monthly print since June 2025, pulling the annual rate down to 3.8% from April's 4.2%. Core CPI — the Fed's preferred signal of underlying price pressures — is forecast to ease only marginally, to 2.8% annually from 2.9%. The numbers underscore a stubborn reality: headline CPI has not dipped below 2.0% since March 2021, and core has remained elevated since April 2021. Moderation is visible, but the destination remains distant.

Read more New Zealand Services Sector Returns to Growth but Recovery Looks Fragile →

The directional implications are relatively clean. A softer print would reinforce the case for the Fed staying on hold before eventually easing, pulling the dollar lower and supporting risk assets. An upside surprise, however, could resurrect rate-hike expectations that markets had largely shelved — a scenario that would lift Treasury yields and the dollar while punishing equities. The binary nature of this setup means positioning into Tuesday carries meaningful uncertainty regardless of conviction.

Warsh's testimony adds a second layer of complexity. He will appear before the House Financial Services Committee on Tuesday at 10:00 AM ET and the Senate Banking Committee on Wednesday. The Fed's prepared Report to Congress, released Friday, described an economy slowing at the household level but buoyed by AI-driven investment and a resilient labor market. The Fed's updated projections trimmed 2026 growth only modestly to 2.2%, while raising headline and core inflation forecasts sharply — to 3.6% and 3.3% respectively — against a projected unemployment rate of just 4.3%. That combination suggests policymakers see little reason to blink on inflation.

The real market risk, however, lies in the unscripted question-and-answer sessions. Warsh has been actively reframing how the Fed communicates, signaling a retreat from the era of explicit forward guidance. Any unguarded remark on rate trajectory — particularly with fresh CPI data on the table — could move markets more than the prepared remarks themselves. Investors would be wise to treat this as a week of two distinct, sequential catalysts rather than a single narrative event. Continue reading at Forexlive.